CBSE Class 12 Accountancy Chapter 13 notes (Computerised Accounting) are detailed and cover Chapter 13 of the syllabus, making them an excellent study tool. CUET Accountancy Chapter 13 Notes are also routinely updated, ensuring that you are receiving the most up-to-date information. The Accounts notes also feature practice questions and answers, allowing you to assess your understanding and discover areas for development.

CBSE Class 12 Accountancy Chapter 13 Notes

Our class 12 accountancy notes for Chapter 13 are intended to help you achieve the greatest possible scores in CUET UG 2026 exam. Subject-matter experts prepare our CBSE Class 12 Accountancy Chapter 13 Notes PDF and feature comprehensive explanations, illustrations, and examples to facilitate learning. Check out Careers Adda’s best CUET crash courses below:

Download CUET Accountancy Chapter 13 Notes PDF for Quick Revision

With our class 12 accountancy notes, you can be confident that you will have the knowledge and abilities required to perform well in your exams. Read the CUET Accountancy Chapter 13 Notes thoroughly to ensure you understand all of the principles. Practice solving problems to better comprehend the material and prepare for the CUET 2026 Exam.

Check our best Careers Adda CUET UG crash courses for Accounts students, to complete the syllabus from our expert faculty.

Accountancy Notes for Chapter 13 – Computerised Accounting

Check the brief Accountancy notes for Computerised Accounting here:

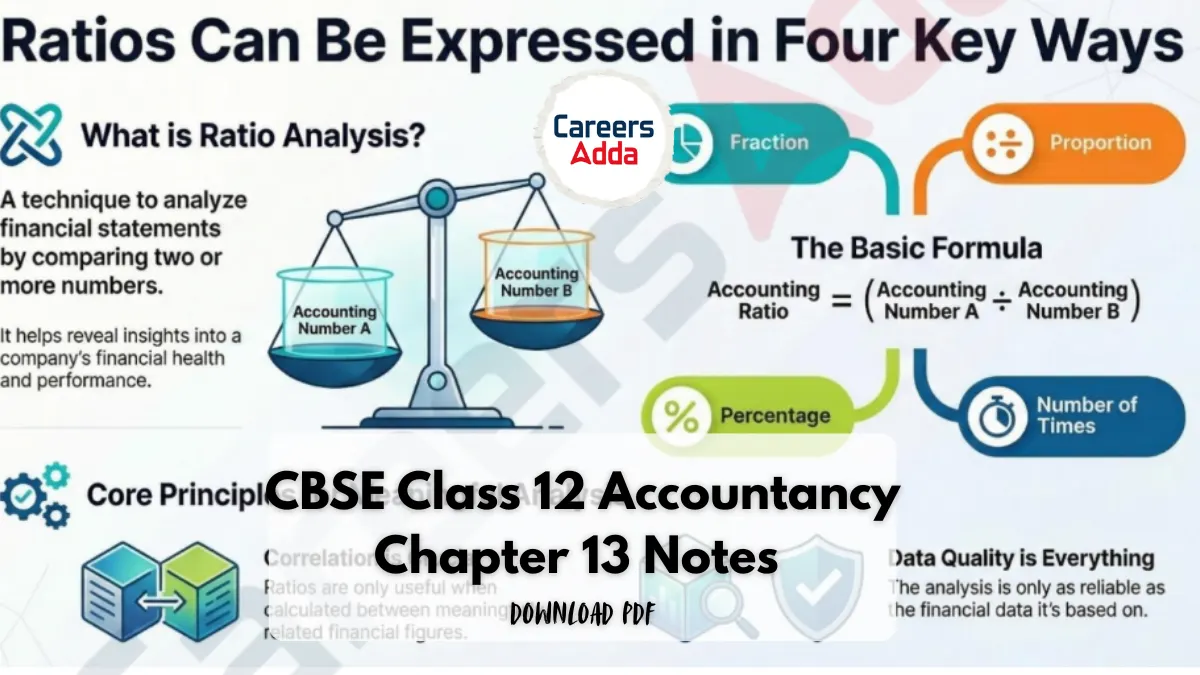

Meaning of Ratio Analysis

Ratio analysis is a technique of financial statement analysis that involves the mathematical calculation of relationships between two or more accounting numbers derived from financial statements.

• Relationship Expression: A ratio can be expressed as a fraction, proportion, percentage, or a number of times.

• Meaningful Correlation: To be useful, ratios must be calculated using numbers that are meaningfully correlated; unrelated figures result in meaningless data.

• Dependence on Data: The efficacy of a ratio depends on the basic numbers; if financial statements contain errors, the derived ratio will be erroneous.

• Formula of Ratios:

o Accounting Ratio = (Accounting Number A ÷ Accounting Number B).

o Percentage Expression = (Numerator ÷ Denominator) × 100.

Objectives of Ratio Analysis

Ratio analysis serves as an indispensable part of interpreting financial results by regrouping data through arithmetical relationships. Its primary objectives include:

• Highlighting Attention Areas: To identify specific sections of the business that require more management attention.

• Identifying Improvement Potential: To locate potential areas where performance can be enhanced with targeted effort.

• In-depth Evaluation: To provide a deeper analysis of the firm’s levels of profitability, liquidity, solvency, and efficiency.

• Cross-sectional Analysis: To compare firm performance against the best available industry standards.

• Projections: To provide information useful for making estimates and projections for the future.

Advantages of Ratio Analysis

Properly conducted ratio analysis improves the user’s understanding of business efficiency and sheds light on latent aspects of the business.

• Decision Efficacy: It helps users understand if the firm has made the right operating, investing, and financing decisions.

• Simplification: It simplifies complex accounting figures and effectively summarizes financial information to assess creditworthiness and earning capacity.

• Comparative Analysis: Keeping multiple years of figures side-by-side, it helps explore visible trends and make projections.

• Problem Identification: It acts as a “whistleblower” by identifying problem areas (weak spots) and bright spots.

• SWOT Analysis: It helps management understand current threats and opportunities, enabling a formal Strength-Weakness- Opportunity-Threat analysis.

• Benchmarking: It allows for various comparisons:

o Intra-firm: Comparison over different accounting periods within the same firm.

o Inter-firm: Comparison with other business enterprises.

o Industry Standards: Comparison against set industry expectations.

Limitations of Ratio Analysis

Since ratios are derived from financial statements, any weakness in the original data is reflected in the analysis.

1. Limitations Arising from Financial Statements

• Accounting Data Precision: Accounting data reflects opinions and personal judgments of accountants rather than absolute facts.

• Price-level Changes: It ignores inflation; a change in the price level makes the analysis of different years meaningless because historical records ignore the decline in the power of money.

• Qualitative Factors: Analysis is limited to quantitative (monetary) aspects and completely ignores non-monetary or qualitative factors.

• Variations in Policies: Differing policies for inventory valuation or depreciation between firms make valid inter-firm comparisons difficult.

Get the Full Accountancy Notes for Chapter 13 from the PDF

CUET UG Business Studies Important Quest...

CUET UG Business Studies Important Quest...

ICSE Result 2026 Out: Class 10 & 12 ...

ICSE Result 2026 Out: Class 10 & 12 ...

JMI Admission 2026 Registration Started,...

JMI Admission 2026 Registration Started,...

Call

Call