Important Questions of Class 12 Accountancy: It’s crucial to revise the key chapters in the comprehensive Class 12 Accounting Syllabus before the CBSE Class 12 Board Exam 2026. Solving these important sample questions will help you comprehend the questions that may arise on the exam. Focusing on relevant Class 12 Accountancy questions streamlines your study efforts and ensures you’re well-prepared for your tests.

Important Questions of Class 12 Accountancy for Board Exam 2026

Learn the Important Questions of Class 12 Accountancy to help you do well on your tests. This post emphasizes central themes and questions you should consider for effective preparation. Practising essential questions will help you prepare for the Class 11 board exams.

CBSE Class 12 Important Accountancy Questions 2026

To help you study more efficiently, we’ve included chapter-specific Class 12 Accountancy Important Questions with solutions in this post. Mastering Class 12 Accountancy is critical for establishing a strong foundation in business. By practicing these Class 11 Accountancy Important Questions, you can increase your comprehension, problem-solving abilities, and confidence.

Important Questions of Class 12 Accountancy for Board Exam 2026 Pattern

| Specifications | Details |

| Exam |

CBSE Class 12 Board Exam 2026

|

| Exam Date | March 28, 2026 |

| Duration | 3 hours |

| Mode of Exam | Offline, Pen and Paper |

| Number of Sections/Parts | 2 (Part A and Part B) |

| Part A |

Question no. 1-26 (Compulsory for all candidates)

|

| Part B |

Question no. 27-34 (Two options i.e. (i) Analysis of Financial Statements and (ii) Computerised Accounting.)

|

| 1 Mark Questions |

Questions 1 to 16 and 27 to 30

|

| 3 Mark Questions |

Questions 17 to 20, 31and 32

|

| 4 Mark Questions | Questions 21, 22 and 33 |

| 6 Mark Questions | Questions 23 to 26 and 34 |

Class 12 Accountancy Important Questions with Answers

Check the important questions for the Class 12 Accountancy exam 2026 below:

Q1. When a partner is given guarantee by other partner, any deficiency on such guarantee will be borne by:

- firm

- all others partners

- partners with highest profit ratio

- partner who has given the guarantee

Q2. Hawan and Pawan are partners in a firm sharing profits and losses in the ratio of 2:3.

Balance Sheet (Extract)

| Liabilities | Amount (₹) | Assets | Amount (₹) |

| Machinery | 1,20,000 |

Machinery is to be depreciated by

- ₹1,20,300

- ₹1,20,000

- ₹1,17,000

- ₹1,10,000

The value of Machinery to be shown in the new balance sheet is:

OR

Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R): Assertion (A): Restructuring of the firm leads to the change in the profit-sharing ratio.

Reason (R): A change in the profit-sharing ratio among the existing partners results in a gain of additional share in the future profits for some partners while a loss of a part thereof for other partners.

In the context of the above two statements, which of the following is correct:

- Both Assertion (A) and Reason (R) are true and Reason (R) is the correct explanation of Assertion (A).

- Both Assertion (A) and Reason (R) are true but Reason (R) is not the correct explanation of Assertion (A).

- Assertion (A) is true but Reason (R) is

- Assertion (A) is false but Reason (R) is

Q3. Divya Ltd. issued fully paid shares of ₹12,00,000 in consideration of net assets of ₹8,00,000. The difference of

₹4,00,000 will be transferred to .

- Surplus A/c

- Capital reserve A/c

- Goodwill A/c

- None of these

OR

Satyam Ltd. forfeited 40,000 equity shares of ₹100 each for non-payment of first and final call of ₹40 per share. The maximum amount of discount at which these shares can be re-issued will be:

- ₹16,00,000

- ₹24,00,000

- ₹40,00,000

- ₹40,000

Q4. On dissolution of a partnership firm, Partners’ Capital Accounts are closed through:

- Realisation A/c

- Drawings A/c

- Bank/Cash A/c

- Loan A/c

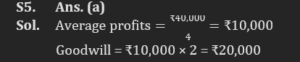

Q5. Goodwill of the firm is to be valued at 2 years’ purchase of the average profit of last 4 years. The total profits for

last 4 years were ₹40,000. Goodwill of the firm will be:

- ₹20,000

- ₹40,000

- ₹10,000

- ₹30,000

Q6. Harish, Prakhar and Sawant were partners in a firm sharing profits in the ratio of 4:3:3. On August 1, 2021, Prakhar died. His 20% share was acquired by Harish and remaining by Sawant. New profit-sharing ratio will be:

- 23: 27

- 27: 23

- 27: 30

- 35: 10

OR

Due to change in the profit-sharing ratio, Anjani’s gain is 1/5th while Hareen’s sacrifice is 1/5th. They decided to adjust the following without affecting their book values, by passing a single adjustment entry:

General Reserve – ₹40,000

Profit and Loss Account (Cr.) – ₹60,000

The necessary adjustment entry will be:

- Debit Anjani’s Capital Account by ₹4,000 and credit Hareen’s Capital Account by ₹4,000.

- Debit Anjani’s Capital Account by ₹20,000 and credit Hareen’s Capital Account by ₹20,000.

- Debit Hareen’s Capital Account by ₹4,000 and credit Anjani’s Capital Account by ₹4,000.

- Debit Hareen’s Capital Account by ₹20,000 and credit Anjani’s Capital Account by ₹20,000.

Q7. If an asset is purchased by a company of ₹11,00,000 and shares are issued @10% premium of ₹10 each to the vendor. How many shares will be issued by the company?

- 1,00,000

- 1,10,000

- 90,000

- None of these

OR

The journal entry to acquire an asset from the vendor for ₹10,000 will be:

| Particulars | Amount Dr. | Amount Cr. | ||

| (A) | Sundry Assets A/c

To Vendor’s A/c |

Dr. | 10,000 | 10,000 |

| (B) | Vendor’s A/c

To Sundry Assets A/c |

Dr. | 10,000 | |

| 10,000 | ||||

| (C) | Sundry Assets A/c To Cash A/c | Dr. | 10,000 | |

| 10,000 | ||||

| (D) | Cash A/c

To Vendor’s A/c |

Dr. | 10,000 | |

| 10,000 | ||||

Read the following case and answer questions 8 and 9 based on the same:

Navin Technologies Ltd. issued 10,000; 9% debentures of ₹100 each at a premium of ₹20 payable as follows:

- ₹40 including premium of ₹10 on application

- ₹40 including premium of ₹10 on allotment

- Balance as first and final

Applications were received for 10,000 debentures and allotment was made to all the applicants. All the calls were made, and amounts received.

Q8. The amount of money received during application is:

- ₹2,00,000

- ₹8,00,000

- ₹4,00,000

- ₹1,00,000

Q9. What amount of the money received on application was transferred to the securities premium reserve account:

- ₹10,00,000

- ₹1,00,000

- ₹2,00,000

- ₹4,00,000

Q10. Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R): Assertion (A): Secret partner participates in the affairs of the management.

Reason (R): Secret partner is not liable to pay debts of the firm.

In the context of the above two statements, which of the following is correct:

- Both Assertion (A) and Reason (R) are true and Reason (R) is the correct explanation of Assertion (A).

- Both Assertion (A) and Reason (R) are true but Reason (R) is not the correct explanation of Assertion (A).

- Assertion (A) is true but Reason (R) is

- Assertion (A) is false but Reason (R) is

Solutions

S1. Ans. (d)

Sol. When a partner gives a guarantee on behalf of the firm or other partners, any deficiency on such guarantee is typically borne by the partner who has given the guarantee. This means that if the guarantee is called upon and there is a financial shortfall, the partner who provided the guarantee will be responsible for covering that deficiency.

S2. Ans. (c)

Sol. The value of Machinery to be shown in new balance sheet

= Machinery – Depreciation

= ₹1,20,000 – (₹1,20,000 × 2.5%) = ₹3,000 = ₹1,17,000

OR

S2. Ans. (b)

Sol. Restructuring of the firm is when there is admission, retirement, death or even just change in the profit-sharing ratio.

S3. Ans. (c)

Sol. Journal Entry: Particulars Amount Dr. Amount Cr.

Assets A/c Dr. 8,00,000

Goodwill A/c Dr. 4,00,000

To Share Capital A/c 12,00,000

OR

S3. Ans. (b)

Sol. Maximum amount of discount at which these shares can be re-issued = Amount standing in the share forfeiture A/c

= 40,000 × ₹60 =₹24,00,000

S4. Ans. (c)

Sol. On dissolution of a partnership firm, Partners’ Capital Accounts are typically closed through Bank/Cash Accounts. This means that any remaining balances in the Partners’ Capital Accounts are transferred to their respective Bank or Cash Accounts as they receive their share of the assets or settlement amount during the dissolution process.

S5. Ans. (a)

Sol.

S6. Ans. (a)

S7. Ans. (a)

Sol. No. of shares issued = ₹11,00,000 = 1,00,000

10+1

OR

S7. Ans. (a)

S8. Ans. (c)

Sol. 10,000 × ₹40 = ₹4,00,000

S9. Ans. (b)

Sol. 10,000 × ₹10 = ₹1,00,000

S10. Ans. (c)

CUET PG LLB Preparation Tips and Strateg...

CUET PG LLB Preparation Tips and Strateg...

CBSE 12th Physical Education Important M...

CBSE 12th Physical Education Important M...

CBSE 12th Political Science Important MC...

CBSE 12th Political Science Important MC...

Call

Call