CBSE Class 12 Accountancy Chapter 9 notes are organized into two sections, each covering a different aspect of the course topic and providing complete solutions to assist students in understanding important accounting concepts. CUET Class 12 Accountancy notes are useful for preparing for exams and establishing a solid foundation in accounting. Accountancy teaches how to handle and record funds for non-profit organizations.

CBSE Class 12 Accountancy Chapter 9 Notes

Cash flow analysis, partnership firms, and financial statements are among the concepts covered in the Class 9 accounting chapter (Analysis of Financial Statements) to help students learn more quickly. Learn the fundamentals of partnership accounting, such as how you handle adjustments when new partners join or old partners depart. CUET Class 12 Accountancy study materials cover the whole syllabus with mock tests, check out now:

Download CUET Accountancy Chapter 9 Notes PDF for Quick Revision

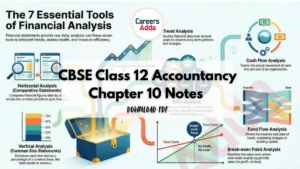

Learn how to analyze financial accounts using a variety of tools and approaches, including accounting ratios from our CUET Class 12 Accountancy Chapter 9 Notes. Learn how to create and understand cash flow statements to track a company’s cash movements. Download the Class 12 Chapter 9 Accountancy Notes PDF from the link below.

Check our best Careers Adda CUET crash courses for Accounts students, to complete the syllabus from our expert faculty.

Accountancy Notes for Chapter 9 – Analysis Of Financial Statements

Check the CUET Accounts Notes for “Analysis Of Financial Statements” below:

Meaning of Financial Analysis

Financial analysis is the process of identifying the financial strengths and weaknesses of a firm by properly establishing relationships between the items of the Balance Sheet and the Statement of Profit and Loss.

• Simplification of Data: Financial statements present complex data in absolute monetary terms; analysis classifies this data into simple, understandable groups.

• Interpretation: It involves “giving tongue to these mute heaps of figures” to reveal information about liquidity, solvency, and profitability.

• Systematic Process: As per Finney and Miller, it consists of separating facts according to a definite plan, arranging them in groups, and presenting them in an easily readable form.

• Comparison: A core feature is making comparisons between various groups to draw meaningful conclusions.

Types or Methods of Financial Analysis

There are two basic approaches used to review and analyze financial data.

1. Horizontal Analysis

• Nature: This involves the review of financial statements for a number of years. This is also called Comparative Analysis.

• Methodology: Figures for two or more years are placed side-by-side to facilitate comparison.

• Dynamic Analysis: Because it is based on year-to-year data rather than a single year, it is termed “Dynamic Analysis”.

• Purpose: It is used to identify trends in sales, cost of production, and profits, highlighting areas of strength or weakness over time.

• Continuous History: It emphasizes that a series of periods is more significant than a single period as it depicts a continuous history of the enterprise.

• Mathematical Representation of Change:

o Change in item = Current Year figure − Previous Year figure.

o Percentage change = (Absolute Change ÷ Previous Year figure) × 100.

2. Vertical Analysis

• Nature: This involves the review of financial statements for a single year or on a particular date.

• Static Analysis: Since it is based on data from a single period, it is termed “Static Analysis”.

• Common Size Statements: It is often presented through “Common Size Statements” where items are expressed as a percentage of a common base.

• Inter-firm Comparison: It is particularly useful for comparing the performance of different companies within the same group or different departments within the same company.

• Tools: This type of analysis frequently utilizes ratios to study quantitative relationships among items in a single period.

• Limitations: It is considered less useful for a proper analysis of a company’s financial position because business is a dynamic process and vertical analysis depends on a single period.

Objectives or Purpose of Financial Analysis

The analysis of financial statements serves several specific goals depending on the needs of the user. The primary objectives are:

• Measure Earning Capacity or Profitability: To ascertain if the business is earning a satisfactory return on invested funds and whether these profits are increasing, decreasing over time.

• Measure Solvency: To determine the ability of the firm to pay short-term and long-term liabilities.

Mathematical focus:

o Short-term Solvency = Current Ratio and Quick Ratio;

o Long-term Solvency = Debt-Equity Ratio.

• Measure Financial Strength: To assess the potential of the business to fund new machinery and equipment from internal resources versus external sources.

• Comparative Study: To help management compare their firm’s performance (sales, expenses, profits) against other firms in the same trade.

• Capability of Payment: To assess if the firm can pay interest consistently and has the capacity to pay dividends at a higher rate in the future.

• Identify Business Trends: To determine the direction (growth, decline) of the business by comparing sales, production costs, and profit margins over multiple years.

• Judge Management Efficiency: To evaluate if the financial policies adopted are proper by comparing actual ratios against standard ratios.

• Identify Weaknesses: To provide information that helps management take remedial measures to remove business weaknesses.

Get the Full Accountancy Notes for Chapter 9 from the PDF

CBSE Class 12 Accountancy Chapter 10 Not...

CBSE Class 12 Accountancy Chapter 10 Not...

Process to Challenge CUET PG 2026 Answer...

Process to Challenge CUET PG 2026 Answer...

Best Books for CUET PG LLB 2027, Check S...

Best Books for CUET PG LLB 2027, Check S...

Call

Call