CBSE Class 12 Accountancy Chapter 7 notes (Issue And Redemption Of Debentures) by our subject-matter experts provide a wide variety of questions, examples, and CUET Commerce practice tests. These Accounts notes break down complex ideas into simple steps, allowing you to understand concepts such as shares, debentures, and critical accounting ratios without difficulty. If you find concepts difficult, these CUET Accountancy Chapter 7 Notes will help you understand them much better.

CBSE Class 12 Accountancy Chapter 7 Notes

CBSE Class 12 Accountancy Part 7 Notes 2026 cover the Issue and Redemption of Debentures analysis. Learning this chapter is made easier with our Careers Adda Class 12 Accountancy Revision Notes. These brief notes can help you remember definitions, important concepts, and solved examples, ideal for last-minute revision or ongoing study.

Download CUET Accountancy Chapter 7 Notes PDF for Quick Revision

Many questions from this CBSE Class 12 Accountancy Chapter 7 Notes are frequently asked in final exams, so revising thoroughly can significantly improve your grade. Careers Adda CUET notes are intended to make you feel confident and ready for your Class 12 Accounting exam.

Check our best Careers Adda CUET Commerce crash courses for Accounts students, to complete the syllabus from our expert faculty.

Accountancy Notes for Chapter 7 – Issue And Redemption Of Debentures

Read the brief highlights of the Accountancy Chapter 7 Notes here:

Meaning of Debentures

The word ‘debenture’ is derived from the Latin word ‘debere’, which means to borrow.

• Definition: A debenture is a written instrument acknowledging a debt under the common seal of the company.

• Contractual Terms: It contains a contract for the repayment of principal after a specific period or at intervals and for the payment of interest at a fixed rate.

• Legal Inclusion: Under Section 2(30) of The Companies Act, 2013, ‘Debenture’ includes debenture inventory, bonds, and any other securities of a company, whether constituting a charge on assets or not.

• Nature of Finance: Funds raised through debentures are known as long-term debt.

Comparison Example: If a company has 1,000 Equity Shares and 1,000, 10% Debentures, both of ₹100:

• Share Capital = 1,000 × 100 = 1,00,000.

• Debenture Debt = 1,000 × 100 = 1,00,000.

• Debenture Interest Cost = 1,00,000 × 10% = 10,000 (Fixed Charge).

• Share Dividend = Dependent on residual profit (Appropriation).

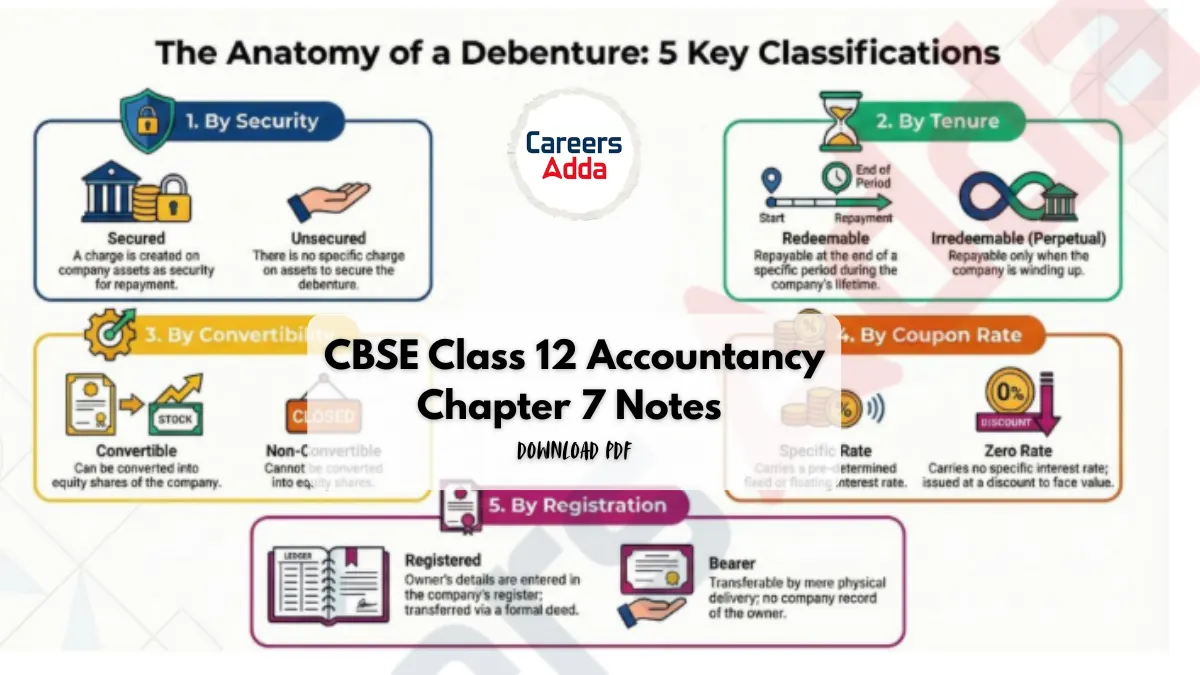

Classification of Debentures

1. From the Point of View of Security

• Secured Debentures: These create a charge on the company’s assets (fixed or floating) to ensure payment in case of default.

o Fixed Charge: Created on specific assets held for use in operations.

o Floating Charge: Created on general assets of the company.

• Unsecured (Naked) Debentures: These do not have a specific charge on the assets of the company.

2. From the Point of View of Tenure

• Redeemable Debentures: These are payable on the expiry of a specific period, either in a lump sum or in instalments.

• Irredeemable (Perpetual) Debentures: The company gives no undertaking for repayment during its lifetime; these are repayable only upon winding-up or after a very long period.

3. From the Point of View of Convertibility

• Convertible Debentures: These can be converted into equity shares or other securities at the option of the company or the debentureholder. They can be fully or partly convertible.

• Non-Convertible Debentures: These cannot be converted into shares or other securities.

4. From Coupon Rate Point of View

• Specific Coupon Rate Debentures: These are issued with a specified rate of interest (fixed or floating). Floating rates are typically tagged to the bank rate.

• Zero Coupon Rate Debentures: These do not carry a specific rate of interest. To compensate investors, they are issued at a substantial discount.

o Total Interest = Nominal Value − Issue Price.

5. From the Point of View of Registration

• Registered Debentures: All details (names, addresses, holding particulars) are entered in the company’s register.

Transfer requires a regular transfer deed.

• Bearer Debentures: Transferable by mere delivery; the company maintains no record of these holders. Interest is paid to whoever produces the interest coupon.

Get the Full Accountancy Notes for Chapter 4 from the PDF

CUET UG Business Studies Important Quest...

CUET UG Business Studies Important Quest...

ICSE Result 2026 Out: Class 10 & 12 ...

ICSE Result 2026 Out: Class 10 & 12 ...

JMI Admission 2026 Registration Started,...

JMI Admission 2026 Registration Started,...

Call

Call