Our thoroughly researched CBSE Class 12 Accountancy Chapter 12 notes are intended to help students get the most out of their tests. Our CUET Chapter 12 accounts notes provide thorough information on the tested topics, with key elements highlighted and discussed understandably. In addition, we use diagrams, charts, and drawings to help people understand complex issues. Download the Careers Adda Accountancy Chapter 12 class 12 Notes PDF and start revising.

CBSE Class 12 Accountancy Chapter 12 Notes

The CBSE Class 12 Accountancy Notes include topics such as financial statement preparation, accounting concepts and procedures, taxation, business law, auditing, and cost accounting. It also helps students prepare for tests like the Chartered Accountant (CA) exam. These CUET Class 12 Accountancy Chapter 12 Notes teach students about financial transactions in business and how to utilize economic models to make educated decisions.

Download CUET Accountancy Chapter 12 Notes PDF for Quick Revision

We provide practice questions and answers to assist students in preparing for the types of questions that may be asked on their exams with the CUET Accountancy Chapter 12 Notes PDF (Cash Flow Statement). We also offer exam-taking advice and methods, such as time management, handling difficult questions, and remaining calm under pressure, at our careers adda website. Get the CBSE Class 12 Accountancy Chapter 12 Notes PDF below.

Check our best Careers Adda CUET crash courses for Accounts students, to complete the syllabus from our expert faculty.

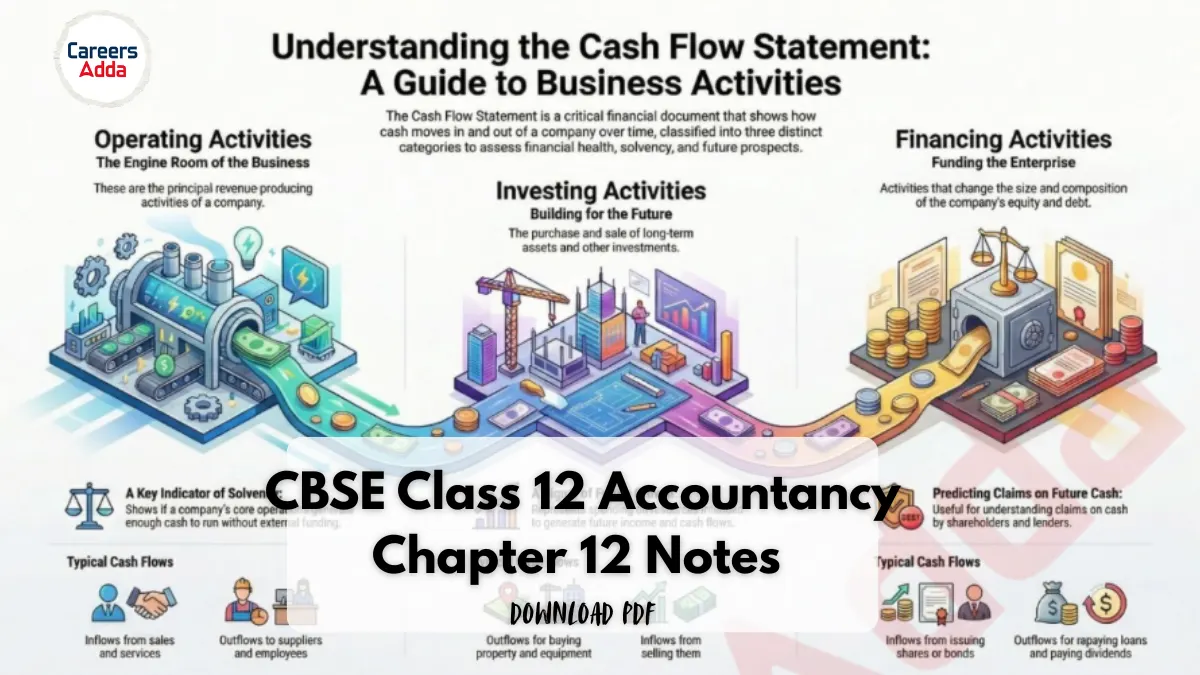

Accountancy Notes for Chapter 12 – Cash Flow Statement

Read the glimpse of the Class 12 Accountancy Chapter 12 Notes for Cash Flow Statement below:

• It is a statement providing information about historical changes in cash and cash equivalents, classified into operating, investing, and financing activities.

• Regulatory Framework: It is prepared in accordance with Accounting Standard-3 (AS-3) as notified under the Companies Act, 2013.

• Key Components:

o Cash: Includes cash in hand and demand deposits with banks.

o Cash Equivalents: Short-term, highly liquid investments readily convertible into cash with insignificant risk of value change.

o Mathematical Criteria: Investment maturity ≤ 3 months from the date of acquisition.

o Cash Flows: Movement in and out due to non-cash items (e.g., Receipt from sale of machinery = Inflow; Payment for machinery = Outflow).

Objectives of Cash Flow Statement

• Activity Breakdown: To provide useful information regarding inflows and outflows under three distinct heads: Operating

+ Investing + Financing activities.

• Generation Assessment: To assess the enterprise’s ability to generate cash and cash equivalents.

• Predictive Value: To evaluate the timing and certainty of cash generation for future economic decisions.

• Utilization Analysis: To identify the needs of the enterprise to utilize those generated cash flows.

Benefits of Cash Flow Statement

• Evaluation of Structure: Enables users to evaluate changes in net assets and the financial structure, including liquidity and solvency.

• Comparability: Enhances the comparability of operating performance between different enterprises by eliminating different accounting treatments for similar transactions.

• Model Development: Allows users to develop models to assess and compare the present value of future cash flows across different businesses.

• Accuracy Check: Helpful in checking the accuracy of past assessments of future cash flows and examining the impact of changing prices.

• Relationship Analysis: Examines the specific relationship between profitability and net cash flow.

• Resource Balancing: Assists in balancing cash inflows and cash outflows in response to changing economic conditions.

Cash and Cash Equivalents

Cash and cash equivalents represent the base components of a Cash Flow Statement, indicating the most liquid assets of an enterprise.

• Cash Composition: Cash = Cash in hand + Demand deposits with banks.

• Cash Equivalents: These are short-term, highly liquid investments that are readily convertible into known amounts of cash.

• Risk Profile: Cash equivalents are subject to an insignificant risk of changes in value.

• Maturity Criteria: Short maturity = 3 months or less from the date of acquisition.

• Inclusions: Cash equivalents = Short-term marketable securities + Short-term deposits + Money-market instruments.

• Exclusions: Investments in shares are generally excluded unless they are preference shares acquired shortly before their redemption date with insignificant risk of failure.

• Mathematical Representation: Total Cash and Cash Equivalents at the end = Net Increase/Decrease in Cash + Cash and Cash Equivalents at the beginning.

Cash Flows

Cash flows involve the movement of cash resulting from transactions with non-cash items.

• Cash Flows = Movement of cash in (Receipts) + Movement of cash out (Payments).

• Cash Inflow: This is the receipt of cash from a non-cash item, such as the sale of fixed assets.

o Example: Sale of machinery = Cash Inflow.

Get the Full Accountancy Notes for Chapter 12 from the PDF

CUET Result 2026 Out: Check Answer Key, ...

CUET Result 2026 Out: Check Answer Key, ...

How to Prepare for Law After Class 12 fo...

How to Prepare for Law After Class 12 fo...

CBSE Class 12 Accountancy Chapter 11 Not...

CBSE Class 12 Accountancy Chapter 11 Not...

Call

Call